Westminster seems to have developed a new national sport.

Over the last decade, we’ve had six Prime Ministers, countless Cabinet reshuffles, enough political drama to fill several box sets, and now another leadership change making headlines.

As a result, one question inevitably lands in our inbox:

“What does this mean for my money?”

The honest answer?

Probably not very much.

That’s not because politics doesn’t matter. It does.

Government decisions can influence Tax policy, spending, borrowing, pensions and regulation. Over time, those things can have an impact on our Financial Plans.

The mistake many people make, however, is assuming that political headlines automatically mean they need to do something with their Investments.

History suggests otherwise.

While politicians come and go, markets are generally far more interested in the bigger picture. Inflation. Interest rates. Economic growth. Corporate profits. Global events.

In fact, what happens in international energy markets or decisions made by central banks can often have a greater influence on Investment returns than whoever happens to be standing outside Number 10.

For now, it’s very much a case of carrying on as normal.

Markets have remained relatively calm following the announcement, which is usually a positive sign. Investors tend to dislike uncertainty, but they also understand that political change is part of the normal cycle of democracy.

One of the biggest advantages of a well-diversified Investment Portfolio is that it isn’t built around one politician, one government or one election result.

It’s designed to navigate change.

That’s important because if the last decade has taught us anything, it’s that political certainty is in rather short supply.

The reality is that there will always be another election, another Budget, another leadership contest and another headline predicting disaster or prosperity.

Very few of them end up changing the long-term direction of a well-constructed Financial Plan.

So whilst Westminster continues its latest round of the hokey cokey, our view remains largely unchanged.

Keep focused on your long-term goals.

Ignore the noise where possible.

And remember that successful investing is usually less about predicting the next Prime Minister and more about sticking to the plan you’ve already put in place.

Most people assume that if they want to put more money into their Pension, they need to earn more first.

Not necessarily.

One of the simplest ways to boost your Retirement savings may already be sitting right under your nose through something called Salary Sacrifice.

Now, before the name puts you off, let’s clear something up.

Despite the word “sacrifice”, this isn’t usually about giving something up and being worse off. In many cases, it’s about getting more money into your Pension without reducing your take-home pay by as much as you might expect.

Here’s how it works.

Instead of receiving part of your salary or bonus and then making a Pension contribution yourself, you agree for your employer to pay that amount directly into your Pension before Tax and National Insurance are deducted.

Why does that matter?

Because neither you nor your employer pays National Insurance on the amount that’s sacrificed.

Many employers also pass some, or even all, of their National Insurance saving into your Pension as an additional contribution, which can give your Retirement savings a meaningful boost over time.

For some people, the benefits go beyond simply building a larger Pension.

Depending on your circumstances, Salary Sacrifice may help:

As with most things in Financial Planning, however, it’s important to look at the bigger picture.

A lower contractual salary can affect other areas of your finances. Mortgage applications, Life Cover, Income Protection and certain workplace benefits may all be linked to your salary level, so it’s important to understand any wider implications before making changes.

The key point is this:

Many people spend years looking for complicated ways to improve their Retirement position, while overlooking opportunities that may already be available through their workplace.

Salary Sacrifice won’t be right for everyone, but where available, it can be one of the simplest and most effective ways to improve the efficiency of your Pension contributions.

Sometimes getting more into your Pension isn’t about earning more.

It’s about making better use of what you’re already earning.

Let’s be honest.

Very few people enjoy thinking about needing care later in life.

It’s one of those topics that often gets pushed into the “I’ll deal with that later” pile, somewhere between updating your Will and finally sorting out that drawer full of old paperwork.

The challenge is that care costs don’t wait for us to feel ready.

With people living longer than ever before, the likelihood of needing some form of care during our lifetime continues to increase. At the same time, the cost of that care continues to rise.

For many families, the biggest concern isn’t simply paying for care.

It’s the fear of losing choice.

Where will I receive care?

Who will make decisions?

Will I become a burden on my family?

Will the money I’ve spent a lifetime building disappear faster than I expected?

These are difficult questions, but they’re important ones.

Many people assume they’ll simply use their savings if care is ever needed. Others expect the value of their home to provide a safety net, or believe that state support will cover most of the costs.

In reality, the answer is often more complicated.

The amount you may need to contribute towards care will depend on your circumstances, assets, income and the type of care required. What works for one family may be completely different for another.

The good news is that there are ways to prepare.

Building up Savings and Investments can provide flexibility. Pensions can play an important role in generating Retirement income. For some people, property wealth may form part of the solution. Others may benefit from specialist planning designed specifically for later-life care needs.

The important thing is not necessarily deciding today exactly how future care would be funded.

It’s understanding what your options might be before you need them.

Because when care becomes necessary, decisions often need to be made quickly and at a time when emotions are already running high.

Good Financial Planning helps create choices.

It helps families understand what resources are available, what potential risks exist, and how different scenarios might affect both lifestyle and Legacy.

None of us can predict whether we’ll need care in the future.

But we can make sure we’re better prepared if we do.

After all, the best time to think about life’s “what ifs” is usually before they become “what now?”

If you were hoping for a dramatic interest rate announcement, this wasn’t it.

The Bank of England has decided to leave interest rates unchanged at 3.75%, joining a growing list of central banks that appear to be taking a cautious “wait and see” approach.

On the surface, that might sound like a non-event.

But interest rates have a habit of influencing far more of our Financial lives than many people realise. They affect Mortgage costs, Savings rates, Business borrowing, Investment markets and, ultimately, the wider economy.

The Bank’s latest decision suggests policymakers are still walking a tightrope.

Inflation has fallen significantly from the levels we experienced a few years ago, which is undoubtedly good news. However, it remains above the Bank’s long-term target, while economic growth continues to look somewhat fragile.

Add global uncertainty, geopolitical tensions and fluctuating energy prices into the mix, and it’s easy to see why policymakers are reluctant to make any bold moves.

So, what does this mean in practice?

For Borrowers, it means immediate relief is unlikely.

For Savers, it means cash deposit rates should remain relatively attractive compared with what we’ve become used to over much of the last decade.

And for anyone approaching the end of a fixed-rate Mortgage, the message remains largely unchanged: rates are no longer rising rapidly, but neither are they falling particularly quickly either.

The reality is that markets were already expecting this decision.

Which highlights an important point.

The biggest market moves rarely happen because of what central banks do. They happen because of the difference between what was expected and what actually happens.

For Investors, that’s an important distinction.

Interest rate decisions will continue to dominate headlines. Financial journalists will analyse every comment, every forecast and every hint about what might happen next.

But long-term Financial Planning isn’t built around guessing the next interest rate announcement.

It’s built around preparing for a range of possible outcomes.

Because whether rates rise, fall or stay exactly where they are, successful planning tends to rely on the same principles: having a clear strategy, staying diversified and avoiding the temptation to react to every headline.

The truth is that nobody knows exactly where interest rates will be in six months’ time.

What we do know is that there will be another Bank of England meeting, another prediction, another headline and another reason for the media to get excited.

For long-term Investors, however, very little has changed.

And sometimes, no change is the story.

Buying a home is supposed to be one of life’s exciting milestones.

In reality, it can sometimes feel more like an endurance event.

Just when you think you’re nearing the finish line, someone pulls out of the chain, a survey throws up an unexpected issue, or another buyer appears with a higher offer and suddenly you’re back where you started.

If you’ve ever been gazumped, you’ll know exactly how frustrating that can be.

After agreeing a price, spending money on surveys and legal work, and perhaps even starting to plan your move, the seller accepts a higher offer from somebody else. You’re left disappointed, out of pocket and wondering why the process feels so fragile.

The Government is hoping to tackle some of these issues through a series of proposed reforms designed to make property transactions more secure.

One of the most significant proposals would introduce legally binding conditional agreements much earlier in the buying process. Once key information about the property has been provided and an offer accepted, it would become much harder for either side to walk away without a valid reason.

There are also plans to require sellers to provide more information about their property before it is marketed. The aim is to give buyers a clearer understanding of what they’re purchasing and reduce the risk of unpleasant surprises appearing later in the process.

In theory, this should mean fewer collapsed sales, fewer wasted costs and greater confidence for both buyers and sellers.

The changes aren’t expected to happen overnight, with reforms likely to be introduced before the end of the current Parliament. However, they represent a significant shift in how the house buying process could work in the future.

And frankly, for many people, that’s long overdue.

Moving home is often one of the largest Financial commitments we ever make. Yet the current system can leave buyers and sellers exposed to uncertainty right up until contracts are exchanged.

Anything that improves transparency, reduces wasted costs and provides greater certainty has the potential to be a positive step forward.

Will it remove all the stress from moving house?

Probably not.

There will still be endless paperwork, last-minute delays, packing boxes that seem to multiply overnight, and that mysterious drawer full of cables nobody is brave enough to throw away.

But if these reforms help more transactions reach completion and reduce the emotional and Financial cost of failed sales, that can only be good news for buyers and sellers alike.

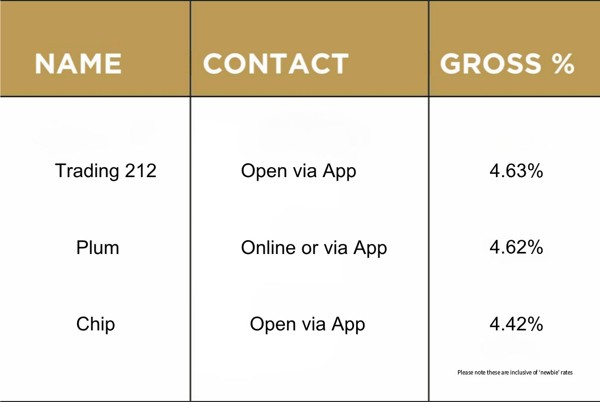

Please check the terms and conditions before opening any account. If in doubt, consult with your financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 30/06/2026

Penguin © 2026. Penguin is a trading name of Penguin Wealth Planners Ltd. who are authorised and regulated by the Financial Conduct Authority (FCA no. 830057). For further information please View More

Customer Focus Award

Customer Focus Award