Wealth Management Update – December 2020

Spending Review: The main points

Chancellor Rishi Sunak has set out what the UK government will spend next year and has given the outlook for the economy.

Here are the points we thought would be of most interest:

- The government has now committed £280bn to get the UK through Covid-19, and public-services Covid funding will be £55bn in 2021/22

- The UK economy is expected to shrink by 11.3% this year, the biggest fall in more than 300 years

- The economy is expected to grow by 5.5% next year and 6.6% in 2022 Output will not return to pre-pandemic levels until the end of 2022

- Borrowing is expected to reach £394bn this year – the highest ever in peace time

- In 2025, the economy could be around 3% smaller than was expected in the March Budget forecast

Whilst the forecast seems bleak, it is clear that 2020 has been a difficult year for most. Although life has been, and in some ways still is, a struggle, it is inevitable that things will get better as time goes on.

Capital tax reform on the way

Earlier this year we mentioned the possibility that the Chancellor may try to recoup some of the debt accrued through the pandemic by increasing tax, and rumour was he had his eye on Capital Gains Tax (CGT).

The rumour mill appears to be correct on this occasion as the Office for Tax Simplification (OTS) has proposed several changes to CGT in what appears to be a rushed report, hinting that the Chancellor may be in a hurry to make significant changes in this area.

CGT is paid only by approximately 1.5 million people and so changes here will affect a smaller proportion of people than would changes to Income Tax or National Insurance. It will, however, have a significant impact on those who are asset owners, shareholders or landlords, and these people are usually (We are generalising here!) in their 50s or 60s and are considered fairly wealthy. The positioning of such an increase to CGT may be that it will affect those who are more able to afford the increase rather than those who are already struggling to make ends meet.

But will an increase in CGT stagnate the market? Will it mean that assets are not disposed of to avoid a tax charge? Or will it cause a mass disposal of assets before the new rules are made official?

A change in terms of simplicity will be welcomed, but we hope the consequences and far-reaching implications of some of the more dramatic changes that have been suggested have been considered in depth.

Bank of England swerves negative interest rates

We touched on this back in June as the world pondered whether the Bank of England (BOE) would be forced to introduce negative interest rates in the UK. The BOE did write to all banks asking them to provide details of how they would manage if interest rates were reduced to 0% or even into negative figures.

If the BOE had decided to dip into negative interest rates it would have raised the possibility that banks will also start to charge savers to hold their cash in current accounts! However, for now, the BOE has instead voted unanimously to increase its purchase of UK bonds by £150 billion and keep interest rates at 0.1%, effectively injecting that cash back into the UK economy. This additional quantitative easing has been implemented by the BOE to support the economy and to try and ease the intensity of the unavoidable slowdown caused by the pandemic.

The BOE stated that the overall outlook for the economy was ‘unusually uncertain’ and would depend heavily on the developments surrounding the pandemic as well as the outcome of talks regarding Brexit. There is some optimism for 2021, where it is expected that Brexit will have a conclusion and restrictions regarding Covid-19 will have been eased.

Beware – Online fraud on the rise

As we have spent the last month in lockdown, not really knowing if normality will return, many of us have turned to online shopping to make sure there are Christmas presents under the tree this year. Sadly, this has resulted in more opportunities for fraudsters to target those looking to bag some bargains in the run-up to Christmas.

UK Finance has said social media platforms, online marketplaces and auction websites are increasingly being used by criminals to carry out these purchase scams, where a customer pays in advance for goods or services that do not exist and are never received. These payments are taken off the integrated payment platform and are made through a bank transfer instead, which means people are unlikely to be refunded.

It has also warned that purchase scams may involve home improvement and DIY purchases, such as patio heaters and sheds, as fraudsters adapt to more people staying at home.

The Take Five to Stop Fraud campaign is urging people to:

Stop: Taking a moment to stop and think before parting with your money or information could keep you safe

Challenge: Could it be fake? It is OK to reject, refuse or ignore any requests. Only criminals will try to rush or panic you

Protect: Contact your bank immediately if you think you’ve fallen for a scam and report it to Action Fraud

Last month, we released a video letting you know about how scammers are on the rise. Click here to watch the video.

Would a Letter of Wishes benefit you?

Although non-binding, a Letter of Wishes (LOW) is commonly used alongside a Will to provide additional details. A LOW is not strictly necessary but there are several situations where it can be beneficial:

If persona chattels are being gifted, listing them in a LOW allows more flexibility than if they were listed in a Will as the LOW can be easily amended at any point. It is, however, worth noting that if a specific gift must go to a specific person, it should be included in the Will as the trustees do not have to follow the LOW.

If you have trusts which give the trustees discretionary powers of management, a LOW can give guidance on how the trust assets should be managed. For example, it could be specified that any grandchildren should only benefit if they go to university.

If you have excluded anyone from your Will who might have a right to make a claim for inheritance, a LOW can explain your reasons for doing so as well as clarifying that this was intentional, to help prevent your Will from being contested. As an administrative benefit, a LOW can show any updated names or addresses since your Will was created so that the contact details remain accurate.

Even if your current Will states your funeral wishes, these wishes are not binding. Funeral wishes can simply be added or updated via a LOW.

A LOW can also clarify guidance for what should happen to your loved ones, and this can include both the care of children and pets to ensure that they are looked after as you wish.

Please get in touch with us if you think that a LOW could benefit you or if you would like to update what you already have in place.

LPAs: Crucial estate planning

The Covid-19 pandemic has starkly demonstrated the importance of having Lasting Powers of Attorney (LPAs) in place. Any of us could find ourselves temporarily incapacitated and in need of help so it is important to know that your wishes for your property, finances, health and welfare will be carried out.

Those are benefits for you – but have you also considered the potential benefits for your loved ones?

Not only will they have the peace of mind of knowing they are carrying out your wishes, but an LPA may also prevent them finding themselves in a position where they cannot effectively manage their own lives. For example, if any of your household bills, bank accounts, insurance, etc. are in solely in your name, if you were to become temporarily or permanently incapacitated then your partner wouldn’t be able to access them … not an ideal situation!

Although the benefits of the standard LPA speak for themselves, if you run your own business are you confident that your wishes regarding the running of the business would be carried out if you became unable to deal with them yourself? If not, there are two simple ways that you can ensure this. If your attorneys and wishes are identical to those in your standard Property and Finance LPA, it can simply be specified that the document covers both your business and your personal affairs. However, if there is a distinction between the two, it may be worth setting up a separate Business and Commercial LPA.

If you want to make changes to your existing LPAs, or if you are considering setting up new ones, one of our advisers will be more than happy to help arrange this.

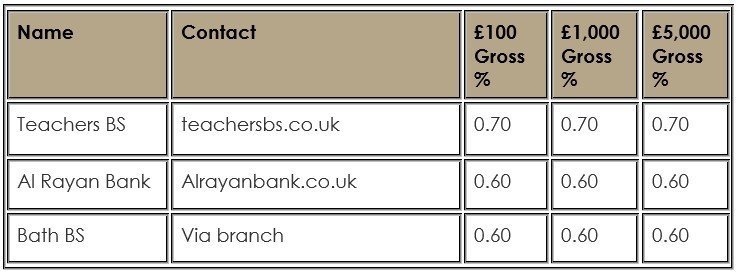

BEST SAVINGS SELECTION

Top three Cash ISAs

Please check with the terms and conditions before opening any account. If in doubt consult with your financial adviser directly as the above are for information only.

Source: Moneyfacts Magazine December 2020 Edition