Wealth Management Update June 2026

Making Tax Digital: Are You Ready for the Changes?

If you’re a Landlord or Self-Employed, there are some important Tax changes on the horizon that are worth being aware of.

HMRC’s “Making Tax Digital” initiative is changing the way Income Tax records are kept and reported. The aim is to move away from paper records, mystery shoeboxes full of receipts, and spreadsheets that only make sense to the person who created them.

From April 2026, anyone with gross business or property income over £50,000 a year will need to follow the new rules. This will extend to those earning more than £30,000 from April 2027.

Rather than submitting everything once a year, affected individuals will need to keep digital records and send HMRC quarterly updates using approved software.

At first glance, that might sound like more admin. However, there may be some benefits too.

Good accounting software can help you stay organised throughout the year, keep track of income and expenses more easily, and reduce the annual scramble to find missing receipts the night before speaking to your accountant.

For those already using bookkeeping software, the transition may be relatively straightforward.

For others who still rely on paper records or spreadsheets, there may be some initial costs and a bit of a learning curve. HMRC estimates average one-off costs of around £320, together with smaller ongoing annual costs.

The good news is that many software providers are expected to offer affordable, and in some cases free, solutions for smaller Businesses and Landlords.

The biggest mistake we often see with changes like this is not the change itself. It’s leaving it until the last minute.

A little preparation now could save a lot of frustration later.

If you’re likely to be affected, it may be worth speaking to your Accountant sooner rather than later so you understand what changes, what software may be required, and what practical steps you need to take.

Like most things in Financial Planning, Tax deadlines have a habit of arriving much faster than we expect.

Inflation Falls… But Don’t Celebrate Too Quickly

There has been some welcome news on inflation recently, with the latest figures showing prices rising by 2.8% over the past 12 months, down from 3.3% previously.

Lower gas and electricity bills have helped ease some of the pressure on households, giving many people a small break from the relentless increases in living costs we’ve experienced over the last few years.

Before anyone gets too excited, however, it’s worth remembering that inflation hasn’t disappeared. Prices are still rising, just at a slower pace than before.

In other words, things are still getting more expensive. They’re simply getting more expensive more slowly.

There are also signs that this improvement may not be permanent.

Ongoing tensions in the Middle East have pushed global oil prices higher, and we’re already starting to see that filter through to fuel costs. Petrol and diesel prices have been creeping up again, which is never particularly welcome when filling the car already feels more expensive than most of us would like.

Businesses are also facing higher transport and production costs. If those costs continue to rise, they often find their way onto shop shelves eventually. Some economists are now forecasting that inflation could move back towards 4% later this year, with food prices remaining under pressure.

The challenge with inflation is that it rarely moves in a straight line.

It is influenced by everything from energy prices and global events to Government policy and consumer behaviour. That makes it incredibly difficult to predict consistently, even for the experts.

For Investors, this is an important reminder that economic headlines will always give us something to worry about.

One month inflation is falling. The next month it may be rising again. Interest rates, oil prices, elections, trade disputes and global conflicts will all take turns dominating the news cycle.

The danger is allowing short-term headlines to drive long-term decisions.

Good Financial Planning isn’t built around guessing what inflation will do next month. It’s built around creating a plan that can cope with uncertainty, because uncertainty is a permanent feature of investing and life.

Markets will continue to react to economic news, just as they always have. But for long-term Investors, staying focused on your goals rather than the latest headline is usually far more productive than trying to predict the next inflation figure.

After all, successful investing isn’t about reacting to every twist and turn. It’s about having a plan that’s designed to work through them.

The Good News? We’re Living Longer. The Bad News? We Need to Pay for It.

The latest figures from the Office for National Statistics suggest we’re all getting pretty good at staying alive.

According to the newest life expectancy projections, girls born in the UK in 2024 are expected to live to around 90 years old, while boys are expected to reach nearly 87. For children born in 2049, those numbers are expected to climb even higher.

At first glance, that’s fantastic news.

Longer lives mean more time with family, more opportunities to enjoy Retirement, and more years to do the things that matter most.

The challenge, of course, is that longer lives also mean our money may need to last much longer too.

In fact, there’s now a very real possibility that many of today’s children could spend more time in Retirement than they do in full-time work. That sounds wonderful until you remember that somebody still needs to fund those extra decades.

The statistics also suggest that reaching 100 years old may become increasingly common. While that’s a remarkable achievement, it creates a very different Financial Planning challenge from the one previous generations faced.

For many people, Retirement is no longer a 10 or 15-year phase of life. A Retirement lasting 25, 30 or even 35 years is becoming far more realistic than many realise.

That’s important because most of the risks people face in Retirement become larger over longer time periods.

Inflation has more time to erode spending power. Care costs become more likely to arise. Markets will experience multiple ups and downs. And withdrawing money from Pensions and Investments for several decades requires careful planning to ensure funds remain sustainable.

This is why good Retirement Planning is no longer simply about reaching Retirement.

It’s about creating a plan that can support the lifestyle you want throughout Retirement.

One of the biggest concerns we hear from clients isn’t dying too soon. It’s living a long life and worrying whether their money will keep up.

The good news is that this is exactly what proper Financial Planning is designed to address.

Because when people ask, “Will I be OK?”, what they’re often really asking is, “Will my money last as long as I do?”

As life expectancy continues to rise, that question is becoming more important than ever.

The Solicitors Regulation Authority Gets Tough

If you’ve recently worked with a Solicitor, opened an Investment, set up a Trust or moved money between accounts, you may have noticed one thing:

Everyone seems to want a lot more paperwork than they used to.

The reason is a continued focus on anti-money laundering regulations, which are designed to make it harder for criminals to move illicit funds through the financial system.

The principle is difficult to argue with. Most people would agree that preventing money laundering is a good thing.

The challenge is that proving where money came from can sometimes feel surprisingly difficult, particularly when the funds are entirely legitimate.

Several years ago, new rules were introduced requiring Solicitors, Financial Advisers, Investment Managers and other regulated firms to carry out enhanced checks on clients and their Source of Funds. Firms were given flexibility around how these rules should be applied, and many developed their own processes and procedures accordingly.

More recently, however, the Solicitors Regulation Authority (SRA) has increased its scrutiny of how firms are applying these rules, leading many Solicitors to tighten their processes further.

As a result, you may find yourself being asked for considerably more information than you would have been asked for a few years ago.

A recent experience brought this home for me.

I was involved in helping purchase our local village pub as part of a Community Pub initiative. Despite knowing the Solicitor for several years, I was still required to complete identity verification checks and provide evidence showing where my contribution had come from.

Simply explaining that the money came from savings built up over time wasn’t enough. To satisfy the requirements, I was asked to provide two years’ worth of bank statements demonstrating how those savings had accumulated.

At the time, I’ll admit it felt a little excessive.

But from the Solicitor’s perspective, they were simply doing what their regulator now expects them to do.

The reason we mention this is because there is a good chance you may experience something similar in the future.

Whether you’re gifting money, investing a lump sum, purchasing a property, settling an Estate, or placing assets into a Trust, you may be asked to provide detailed evidence showing exactly where funds originated.

If that happens, try not to take it personally.

It isn’t because you’ve done anything wrong.

More often than not, it’s simply because regulated firms are under increasing pressure to demonstrate that they’ve carried out appropriate checks and can evidence them if challenged by their regulator.

Like many areas of modern life, the paperwork may be frustrating, but it’s increasingly becoming part of the process.

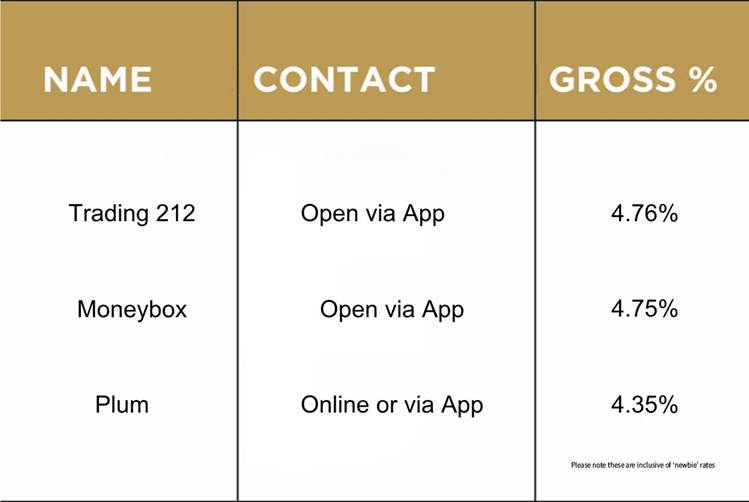

Top three cash ISAs

Please check the terms and conditions before opening any account. If in doubt, consult with your financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 28/05/2026