Wealth Management Update April 2026

How global events can affect your money

Trump strikes again. The US and Israel launched coordinated strikes against Iran following rising tensions around its nuclear programme. Iran has since responded with retaliatory attacks, and the situation remains uncertain at the time of writing.

It can feel like events like this are far removed from everyday life in the UK, but they often have a direct impact on our Finances.

One of the first places people notice it is petrol prices. Costs at the pump have been rising, and if oil prices stay high, they could increase further. Higher fuel costs also tend to push up the price of transporting goods, which can make everyday items more expensive.

Mortgages are also being affected. Earlier in the year, there was an expectation that interest rates might fall quite significantly. However, at its most recent meeting, the Bank of England decided to hold rates. As a result, Mortgage rates have started to edge up again, and some deals have been withdrawn. Borrowing could therefore be more expensive for now, and there may be less choice available.

Looking ahead, expectations have shifted. Any rate cuts now look likely to be smaller than first thought, and there is a chance they may not happen at all in the near term.

Energy bills are a bit more uncertain. Prices are due to fall slightly in the short term, but what happens later in the year will depend on wider energy costs. If those remain high, bills could rise again.

This is a great example of how events around the globe can impact us here at home. With Trump and his associates now under scrutiny for potential insider trading after traders bet hundreds of millions of dollars on oil contracts just minutes before US President Donald Trump announced on Monday that the US would postpone strikes against Iranian energy infrastructure, the situation gives off Trump’s usual scent of duplicity and drama!

If you’d like to explore this topic in a bit more detail, we recently shared a related article with our clients. You can read it here: https://conta.cc/3PTzDOO

And if your Mortgage is due for renewal in the next 6–12 months, it’s worth getting ahead of things early. Feel free to email our Mortgage Adviser, Chris, to look at your options: [email protected].

What the spring statement means for you

The latest Spring Statement from Rachel Reeves was fairly low key, with no major Tax rises or spending changes announced. However, it still gives us a useful snapshot of where the UK economy might be heading.

One of the key updates was around economic growth. The forecast for this year has been slightly downgraded to 1.1%, meaning the economy is expected to grow, just not as quickly as previously hoped. Looking further ahead, growth is expected to improve gradually over the next few years.

Inflation, which measures the cost of living, is expected to average around 2.3% this year before settling back to the government’s 2% target by 2027. That suggests things should continue to stabilise, although global events could still affect this.

Interest rates are another area to watch. Mortgage rates are expected to edge up slightly over time, rather than fall sharply. This reflects ongoing uncertainty and means borrowing could remain a little more expensive than many had hoped.

There are also some mixed signals around jobs and housing. Unemployment is expected to rise slightly in the short term before improving later on. Housebuilding is forecast to dip before picking up again towards the end of the decade.

The Government’s Finances are broadly in line with expectations, with a bit more flexibility than previously forecast. However, recent global tensions, particularly in the Middle East, mean the outlook remains uncertain.

The main takeaway is that while things are relatively stable for now, the pace of improvement may be slower than expected, so keeping plans under regular review remains important.

Could your ISA make you a millionaire

It might sound surprising, but there are now more ISA millionaires than lottery millionaires in the UK. And the gap is only expected to grow.

Figures from HMRC show there are already thousands of people with over £1 million in their ISAs, with many more not far behind. In fact, tens of thousands of Investors are sitting on pots between £500,000 and £1 million. With time and steady growth, many of them are expected to cross the million-pound mark over the next decade.

The key difference compared to the lottery is simple. This is not about luck. It is about consistency.

ISAs allow you to save or invest up to £20,000 each year, with no Income Tax or Capital Gains Tax to pay on growth. Over time, that Tax efficiency can make a big difference, especially if you stay invested and let compounding do the heavy lifting.

It is also worth noting that not all ISAs are the same. Cash ISAs can be useful for short term Savings or emergency funds, but they are unlikely to deliver the kind of growth needed to build significant long-term wealth. Many of the ISA millionaires have built their pots through Stocks and Shares ISAs, which come with more ups and downs but greater long-term potential.

Another advantage is flexibility. Unlike Pensions, you can access your ISA whenever you need to, with no Tax to pay on withdrawals.

Our take at Penguin

ISAs are a powerful tool, particularly for building accessible, Tax-efficient wealth over time. But it is important to look at the bigger picture.

In many cases, those same Investors could have been even better off if they had directed some of that money into their Pensions instead, especially if contributions were made from gross income before Income Tax.

That upfront Tax relief can significantly boost the amount being invested from day one, giving compounding even more to work with over time. For many people, this can make a meaningful difference to long-term outcomes, particularly when planning for Retirement.

The real value comes from using both ISAs and Pensions in the right way, at the right time. One offers flexibility and access, the other offers powerful Tax advantages and long-term growth potential.

The takeaway is not that everyone will become an ISA millionaire. But it does show what is possible with regular Investing, patience and the right approach, and that the structure you use can be just as important as the amount you Invest.

Why property paperwork is taking longer than expected

If you are currently dealing with any changes to property ownership, you may notice that things are taking longer than usual. This is largely down to delays at HM Land Registry, who are currently experiencing a backlog across a number of applications.

One common example is a transfer of equity, where ownership of a property is shared or passed to another person. These applications are currently taking at least six to eight months to be completed, and in some cases even longer.

Another area seeing delays is the first registration of a property. This usually applies to properties that have not previously been registered, and the process can now take around two years. In many cases, the application may not even be reviewed until that point, which can extend timelines further if additional information is needed.

You may also come across something called a severance of tenancy, which is often used in Estate Planning. While the official timeframe can be quoted as up to 18 months, in practice it is often completed within six to nine months. Importantly, the legal change itself takes effect as soon as the relevant notice is signed, even if the Land Registry update takes longer.

The key thing to understand is that these delays are administrative rather than legal. In many cases, your arrangements are already in place, and the Land Registry is simply catching up with recording them.

While it can be frustrating, it is worth allowing extra time and avoiding unnecessary worry if you do not see immediate progress.

Your digital life and digital legacy can be just as important as your physical assets.

When people think about Estate Planning, they usually focus on things like Property, Savings and Investments. But there is another area that is often overlooked, and it could be just as important to your family.

Your digital life.

This includes everything from photos and videos to email accounts and online storage. Unlike physical assets, these are not always easy to pass on. In many cases, access is controlled by the terms and conditions of the provider, rather than standard inheritance rules.

A recent case brought this into focus across numerous news outlets. Rachel Thompson spent three years trying to access her late husband’s iCloud account, which contained thousands of family photos and videos. Despite being the Executor of his Estate, she was initially denied access and only succeeded after a lengthy legal process.

Situations like this are more common than you might think. Many people assume their loved ones will automatically be able to access their accounts, but that is not always the case.

The challenge is that technology companies must balance privacy with access. Without clear instructions, they may refuse requests, even from close family members.

The good news is that this is something you can plan for. Simple steps such as keeping a secure record of your accounts, noting how you would like them handled, and making sure the right people know where to find this information can make a big difference.

Taking a little time to organise your digital life can help avoid unnecessary stress and ensure important memories are not lost.

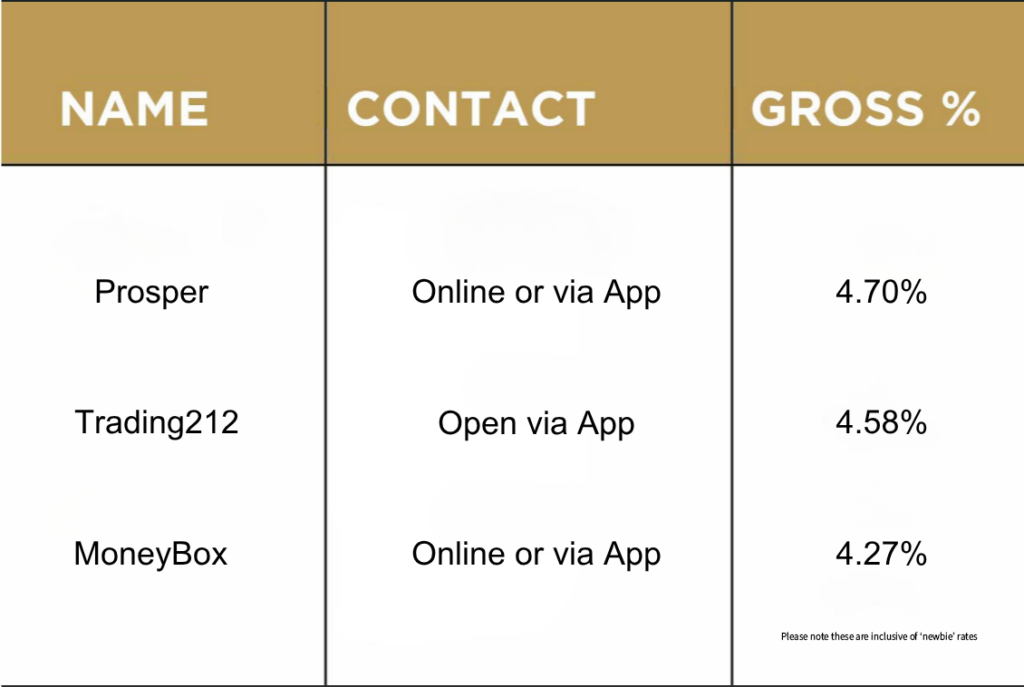

Top three cash ISAs

Please check the terms and conditions before opening any account. If in doubt, consult with your financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 02/04/2026