Wealth Management Update March 2026

Easter Squeeze: Tax year end is closer than it looks

We know we mentioned Tax year end last month, but we thought an extra reminder about the timescales was needed. With the Easter weekend falling right at the end of the Tax year, there are fewer working days than usual to put plans in place before 5 April. This means investment providers, platforms and Pension companies are likely to be busier and cut-off points for contributions may fall earlier than you expect.

Our recent Tax Briefing was a great success – thank you to everyone who attended and for the thoughtful questions that were raised during the session.

If you’re planning to use ISA allowances, make Pension contributions, or carry out any other Tax year end planning, please don’t leave it until the last minute. We recommend confirming instructions with us as soon as possible to avoid missing deadlines.

The last working day before the Easter Bank Holiday is Thursday 2 April, so don’t delay.

State Pension rises again. But how long will it stay Tax-free?

The State Pension is increasing once more, with the full new State Pension rising by 4.8% to £12,547 per year and the Basic State Pension increasing to £9,607 per year.

On the face of it, that’s positive news. The annual uplift helps Pensioners keep pace, at least partly, with the rising cost of living. Thanks to the “triple lock” system, the State Pension increases each year by the highest of inflation, wage growth or 2.5%, which has delivered meaningful rises in recent years.

For many retirees, the full new State Pension now sits just below the current Personal Allowance of £12,570. In simple terms, that means someone with no other income can receive their State Pension free of Income Tax.

But this is where things get interesting.

Income Tax thresholds are currently frozen until April 2031. As the State Pension continues to rise each year, it edges ever closer to and could soon exceed, the Personal Allowance. If that happens, some Pensioners who rely mainly on the State Pension could find themselves paying Tax on part of it.

Add in even modest additional income, perhaps from a private Pension, part-time work or savings interest and the Tax position changes further.

This is a classic example of fiscal drag in action. Pension income increases, but Tax thresholds stand still, gradually pulling more people into the Tax net.

For now, many retirees can enjoy a State Pension that sits just under the Tax threshold. But with ongoing increases built into the system, that position may not last forever.

Premium Bonds: lower prize rate and longer odds

Premium Bonds remain one of the UK’s most popular savings products, but from April 2026 the numbers are changing.

The prize fund rate is being reduced from 3.60% to 3.30% and the odds of each £1 Bond winning a prize will lengthen from 22,000 to 1 to 23,000 to 1. In simple terms, that means slightly fewer prizes overall and a marginally lower average return for savers.

Premium Bonds don’t pay interest in the traditional sense. Instead, the prize fund rate determines how much is paid out across the monthly draws. Every £1 Bond is entered into the draw each month, with prizes ranging from £25 to £1 million. The headline attraction, of course, is that all prizes are Tax-free.

The two £1 million jackpots will remain each month. However, at other prize levels, such as £100,000, £50,000 and £1,000, the expected number of prizes will fall slightly from April 2026. Overall prize numbers are projected to drop from just over 6.1 million in February 2026 to around 5.9 million in April.

The change reflects wider movements in the savings market, where rates have been gradually adjusting. For savers, it’s a reminder that while Premium Bonds offer security and flexibility, with up to £50,000 allowed per person, returns are never guaranteed.

For some, the appeal is the excitement and the chance of a large, Tax-free win. For others, especially those seeking predictable income, traditional savings accounts may be more suitable. As with any savings decision, it comes down to balancing certainty, accessibility and the possibility of a prize.

Why small spends are costing more

When people think about Inflation, they often picture big-ticket costs like fuel, energy bills or Mortgage payments. But Inflation doesn’t just hit the obvious expenses. It also shows up in the small, everyday purchases that slip under the radar.

This reflects a steady rise in the cost of coffees, meal deals, snacks, fast food and other little pick-me-ups. Individually, the increases may only be 10p, 20p or 30p. But over time, they reflect the broader impact of Inflation across the economy.

Food and non-alcoholic drink prices have risen by around 4.5% year-on-year. Higher ingredient costs, wage increases and supply chain pressures all feed through to the price you pay at the till. That’s why a £1.50 fast-food item is now closer to £2, or why your usual lunchtime meal deal has quietly edged up again.

The impact becomes clearer when you multiply it out. A £4 coffee bought three times a week costs more than £600 a year. If Inflation pushes that up, you’re paying noticeably more over 12 months, without changing your habits at all.

This is how Inflation erodes spending power. Your income may stay the same, but the cost of maintaining the same lifestyle gradually increases. Inflation isn’t always dramatic – but it is persistent and the cumulative effect is what really counts.

Salary versus dividends: what’s the difference?

If you run your own limited company, one of the key decisions is how to pay yourself – salary, dividends, or a combination of the two. While both put money in your pocket, they’re Taxed very differently.

Salary is treated as earned income. It’s subject to Income Tax at 20%, 40% or 45% depending on your total income. Employee National Insurance (NIC) is also due at 8% on earnings between £12,570 and £50,270 and 2% above that. On top of this, the company may need to pay employer’s NIC at 15% on earnings above £5,000, although the Employment Allowance can sometimes reduce or cover this cost.

Dividends work differently. They’re paid from company profits after Corporation Tax has already been deducted. Individuals benefit from a £500 dividend allowance (2025/26). Beyond that, dividends are Taxed at 8.75% for basic rate Taxpayers, 33.75% for higher rate and 39.35% for additional rate Taxpayers. Importantly, dividends don’t attract National Insurance.

There’s also a company Tax angle. Salary (and employer’s NIC) is deductible for Corporation Tax purposes, which can mean a saving of up to 25% depending on the company’s profit level. Dividends are not deductible, as they’re paid from retained profits.

Long-term planning matters too. Receiving a salary at or above the Lower Earnings Limit (£6,500 in 2025/26) secures a qualifying year for State Pension purposes and 35 qualifying years are needed for the full entitlement.

In reality, many Business Owners use a blend of salary and dividends. The right balance depends on personal income levels, company profits and longer-term Financial goals.

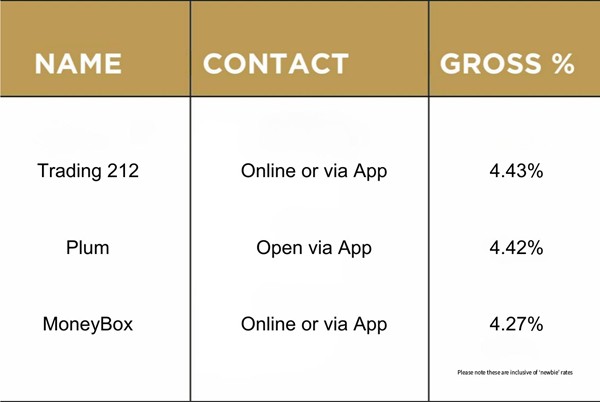

Top three cash ISAs

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 02/03/2026