Wealth Management Update Christmas Special 2025

Budget 2025: What’s Changing, What It Means, and Why It Matters

The Budget has landed – and with it, a mix of headlines, speculation and a few early leaks courtesy of the Office for Budget Responsibility. But once the dust settles, what really matters is how these changes impact you.

We’ve pulled together the key measures you need to know about – the good, the not-so-good and what to keep an eye on over the months ahead.

Property & Estate Planning

Mansion Tax Introduced (April 2028)

A new Council Tax surcharge – dubbed the “Mansion Tax” – will apply to properties valued between £2m and £5m.

• £2,500 per year for homes over £2m

• £7,500 per year for homes over £5m

A full consultation is expected next year.

Business Relief – Spouse Transfer Allowed

From April 2026, the £1m Business Relief for Inheritance Tax will become transferable between spouses, adding greater flexibility to Estate Planning.

Taxation & Income

Tax Bands & National Insurance – Frozen Until 2031

While there’s no headline tax increase, frozen thresholds mean more of your income could be taxed as wages rise with inflation. Since 2021-22, this has equated to a 25% real-terms tax rise.

Dividend Tax & Property Income Tax Increases (April 2026/27)

• Dividend Tax increases by 2% for basic and higher-rate taxpayers – to 10.75% and 35.75% respectively

• Property Income Tax on personally held properties rises by 2% – to 22% basic rate, 42% higher rate and 47% additional rate

• Dividends and property income held in limited companies are currently unaffected

Savings & Investments

ISA Allowance Rebalanced (From April 2027)

• Total annual allowance remains £20,000

• Under-65s: Only £12,000 can go into a Cash ISA – the rest must be in a Stocks & Shares or Investment ISA

• Over-65s: Can continue to use the full £20,000 in a Cash ISA

Junior ISAs and Lifetime ISAs remain unchanged

VCT Tax Relief Cut (April 2026)

• Income Tax relief on Venture Capital Trusts drops from 30% to 20%

• Tax-free growth and dividends remain intact

Employee Ownership Trusts (EOTs)

• Capital Gains Tax relief reduced from 100% to 50% – meaning lower net proceeds for business owners selling via EOTs

Pensions & Benefits

State Pension Rises (April 2026)

• Increases by 4.8%

• Government says Pension Income will be Tax-free, but details are not yet clear

Salary Sacrifice Pension Cap (From April 2029)

• National Insurance exemption capped at £2,000 per year (equivalent to ~£166/month contributions)

• Higher earners and businesses using this structure will see reduced savings

Two-Child Benefit Cap Removed (From April 2026)

• Families with more than two children will once again receive Child Benefit for all children

• This offers meaningful support but may increase long-term government spending

Everyday Costs

Fuel Duty Rises & New EV/Hybrid Charges

• Driving becomes more expensive as fuel duty increases and electric/hybrid vehicle charges are introduced

• Aimed at encouraging more efficient travel, but will raise costs for many

What Wasn’t Touched?

It’s worth noting that many areas remain unchanged, including:

• Income Tax rates

• Capital Gains Tax

• Inheritance Tax thresholds

• Pension allowances

• Stamp Duty

• Main Residence CGT relief

So, What Should You Do Next?

If any of these changes affect you – or you’re unsure whether they do – we’re here to guide you. As always, we put your goals at the centre of your planning.

Whether you’re concerned about future Tax bills, Estate Planning, or how your Investment strategy stacks up under the new rules, we can help you take practical next steps.

Here’s how to connect with us:

Watch Our 2025 Budget Briefing

You can now watch our full 30-minute Budget Briefing online, where we walk through the key announcements and what they really mean for your Financial Plans – in plain English.

Watch now on YouTube

Planning Meetings – For Clients

Book your FP meeting to review your plan in light of the Budget – it’s all part of your ongoing service.

The Penguin Perspective

Planning isn’t about reacting to headlines. It’s about building a strategy that can flex with change – and still deliver on your long-term goals.

We’ll continue to monitor the finer details and keep you updated. In the meantime, stay calm, stay focused – and know we’re here to help every step of the way.

FSCS protection is increasing

There’s some good news for savers. From 1 December 2025, the Financial Services Compensation Scheme (FSCS) increased the amount of protection available on bank and building society deposits. This update follows confirmation from the Prudential Regulation Authority (PRA) and comes after months of consultation (and a fair bit of speculation!).

The standard FSCS limit will rise from £85,000 to £120,000 per person, per Financial institution, a sizeable jump of just over 41%. This is higher than the PRA originally proposed earlier in the year, thanks to updated inflation data showing how much the cost of living has moved since the old limit was set back in 2017.

There’s also an uplift to the Temporary High Balance (THB) protection, which covers larger deposits linked to major life events, such as receiving an inheritance, a property transaction or an insurance payout. The limit will increase from £1 million to £1.4 million, still protected for six months from the date the money hits your account.

A useful reminder, FSCS protection applies per customer, per banking licence, not per brand. So, if two banks share a licence (for example, Halifax and Bank of Scotland), your combined deposits across them count as one pot for FSCS purposes. On the plus side, joint accounts will benefit from £240,000 of protection from 1 December.

Banks and building societies have until May 2026 to update their documents, but the increased protection takes effect this year.

In reality, will the UK Government let another institution fail after the 2008 debacle…probably not but peace of mind for some.

Avoiding common LPA mistakes

Lasting Powers of Attorney (LPAs) are incredibly valuable documents, but they’re also far more technical than most people expect. Every year, we help clients register LPAs, and we regularly see how easily small, innocent mistakes can lead to delays, queries from the Office of the Public Guardian (OPG), or complete rejection. With LPAs, accuracy truly matters, which is why we always recommend having them prepared and overseen professionally.

One of the most common problem areas is dating. LPAs must follow a strict sequence of signatures, and even a slightly unclear number (a 5 looking like an 8, for example) can create issues. Overwriting is not allowed, so if there’s a mistake, the page has to be reprinted and re-signed. The same applies to continuation sheets, which must be dated before or on the day the donor signs their part.

We also see frequent issues with signatures, either placed outside the signature box, marked with pencil, or witnessed incorrectly. Even witnesses need to get it right: full names (including middle names), proper addresses, and signing in the right place are all essential. Using abbreviations for overseas addresses is another reason we’ve seen the OPG reject documents.

Another trap is manual amendments. These must be initialled perfectly to be valid, and even then, the safest approach is usually to have a clean page reissued. Section 12 and Section 15 also have very specific rules; only the correct registering party should complete them, and attorneys must not sign where the donor is responsible for registration.

Finally, when LPAs are posted out for remote signing, it’s surprisingly easy for pages to be mixed between the Property & Financial Affairs LPA (LP1F) and the Health & Welfare LPA (LP1H).

LPAs offer huge peace of mind, but the signing process is unforgiving. A professionally drafted and supervised LPA avoids these pitfalls, protects your intentions, and ensures everything is registered smoothly the first time.

Contact us if you haven’t put this important Planning in place yet – [email protected].

Pension provider problems post-death

A recent case reported in the Financial press highlights just how difficult things can become for families when Pension providers request additional paperwork after someone has passed away. It’s a reminder of why good Planning and having professional support can make a huge difference at an already emotional time.

Mrs P, a widow living in Canada, notified Aviva of her husband’s death back in March 2025 and provided a valid death certificate. However, because the certificate didn’t state the cause of death, Aviva refused to release her late husband’s Pension benefits. Instead, they requested a separate document from a Canadian doctor confirming the cause of death, and insisted it be posted in its original hard-copy form, rather than emailed.

This left Mrs P waiting eight months for the benefits she was entitled to, even though another UK Pension provider holding one of her husband’s other Pensions processed its claim smoothly without demanding a medical confirmation.

Aviva stated that its process was due to “reporting standards” and the need to confirm whether the death involved any third-party factors, accidents or suicide. After pressure from Mrs P’s advisers, Aviva eventually agreed to accept the cause-of-death confirmation by email and has since waived the requirement for it to come from a medical professional, so long as the adviser can verify it.

For families dealing with bereavement, situations like this can be distressing and confusing. Pension death benefit claims can vary dramatically between providers, and requirements aren’t always consistent or clearly explained.

This is exactly why we encourage clients to inform us as early as possible of a bereavement, so that we can provide as much support as we can in such a difficult time.

Bank of England holds rates at 4% – what it means and what might happen next

The Bank of England has kept interest rates at 4% again as it continues trying to steer inflation back toward its 2% target. Inflation has been stubbornly above that level for some time, and the Bank is trying to strike a balance between cooling price rises and not putting too much strain on an already sluggish economy.

The base rate matters because it directly influences the cost of borrowing and the reward for saving. When the Bank raises or cuts its rate, banks and building societies usually adjust their mortgage, loan and savings rates in response. So even small movements can affect millions of people.

Over the past few years, we’ve been on quite a journey. After climbing to 5.25% in 2023, the base rate has been steadily reduced through 2024 and 2025, eventually landing at 4% in August. Since then, the Bank has chosen to hold steady at its September and November meetings.

Inflation has eased from the double-digit highs we saw in 2022, but it’s still higher than policymakers would like. The latest CPI figure, 3.6% in the year to October, shows prices are rising, just not quite as fast as before. Rising food prices remain a key driver.

Looking ahead, many analysts believe we could see a rate cut as soon as the next meeting on 18 December. At the last vote, four out of nine policymakers wanted to cut rates, so sentiment is clearly shifting. Upcoming Budget announcements and global economic conditions, including the impact of US tariffs, may also influence the Bank’s next move.

For now, the message is: rates are stable but could start to edge down. As always, we’ll keep you updated.

The UK economy shows signs of life

There’s finally some good news on the economy front, the UK grew by 0.6% in the third quarter, according to the latest official figures. It’s the strongest growth we’ve seen for over a year and a clear sign that things might be turning a corner after a sluggish spell.

What’s driving it? A mix of stronger consumer spending, falling inflation and a small bounce in services like hospitality and construction. Businesses are still cautious, but there’s a growing sense that the UK has managed to dodge a deeper downturn. That doesn’t mean we’re in boom territory, but it’s a welcome bit of stability after months of stop- start growth.

For savers and Investors, this matters. A steadier economy could help to anchor inflation further, which in turn might make it easier for the Bank of England to start cutting Interest Rates next year. That could bring a little relief to anyone with a Mortgage and may nudge markets into a slightly more optimistic mood.

However, it’s still a mixed picture. Prices are rising more slowly, but they’re still rising; and wage growth, while cooling, remains high enough to keep policymakers cautious. The Bank won’t want to loosen policy too early and risk another Inflation surge.

For now, think of it as a cautious step in the right direction. The UK economy is showing resilience, businesses are adapting and consumers are still spending, just more selectively.

Mortgage rates creep higher – what’s going on?

After months of slow and steady falls, Mortgage rates have started creeping up again. At the time of writing, according to the latest data, the average two-year fixed deal has risen to just under 5%, while the average five-year fix now sits around 4.8%. It’s not a dramatic surge, but it’s a clear sign that the downward trend we’ve seen since early summer may be stalling for now.

So, what’s behind the rise? A lot of it comes down to expectations about the Bank of England. Markets had been betting that Interest Rates would start coming down soon, but with Inflation still proving stubborn, those hopes have been pushed back. As a result, the cost for lenders to borrow money and therefore the cost they pass on to borrowers, has edged higher.

For homeowners coming to the end of a fixed-rate deal, this could mean slightly higher monthly repayments than they’d been hoping for. And for anyone looking to buy, it’s another reminder that timing really matters in today’s market. Even a small change in rates can make a noticeable difference over the term of a mortgage.

That said, it’s not all doom and gloom. The housing market is proving more resilient than many expected and lenders are still competing for business, meaning there are deals worth shopping around for.

As always, the key is not to panic but to plan. If your Mortgage is due for renewal in the next six to twelve months, it’s worth reviewing your options early.

A good rule of thumb is to start reviewing your rate around six months before your deal ends – and if you’d like a no-obligation review of your options, just get in touch – [email protected].

LPA fees set to rise – here’s what you need to know

If you’ve been thinking about setting up a Lasting Power of Attorney (LPA), now’s a good time to get started. On 17th November 2025, the Office of the Public Guardian (OPG) increased the fee to register an LPA from £82 to £92 per application.

That’s a £10 rise per document, which may not sound like much, but most people choose to register two LPAs, one for property and Financial affairs and another for health and welfare. For couples doing both, the total goes from £328 to £368, so it’s worth acting before the change if you can.

For context, these fees are set by the OPG, not by Advisers or Solicitors and we unfortunately have no control over them. The increase reflects administrative costs and government efforts to modernise the LPA process, including the move toward a new digital system.

If you’re not familiar with LPAs, they allow you to appoint trusted people (known as attorneys) to make decisions on your behalf if you lose mental capacity. Having one in place ensures your Finances and care preferences are handled smoothly, without the need for lengthy court applications later.

If you’ve already completed your LPA paperwork but haven’t yet registered it, it’s worth considering submitting the forms as soon as possible to secure the current £82 fee.

And if you haven’t yet started the process, we can help point you in the right direction to get them set up.

Do your Pensions count towards care costs?

It’s a question that comes up time and again, if you ever need long-term care, will your Pension be taken into account when the local authority works out how much you should pay?

The short answer is not usually, at least while your Pension remains untouched (uncrystallised). In most cases, your Pension pot isn’t counted as a capital asset when the council does its means test. However, any income you’re taking from it will be included, so if you’ve started drawdown or are receiving an annuity, that income can affect how much help you get.

Once you reach State Pension age, things get a bit more complicated. Even if you’re not drawing from your Pension, the local authority can assume a “notional income” — in other words, they may assess you as if you were taking a Pension income, based on what someone your age could reasonably receive.

That’s why planning ahead really matters. Leaving Pensions untouched can be a useful strategy for keeping funds out of the care assessment, but from 2027, uncrystallised Pensions will become subject to Inheritance Tax (IHT) when passed on after death. So, while keeping your Pension “until last” has often been seen as a smart move, this change may reduce some of that advantage (though the details are still being finalised).

As ever, there’s no one-size-fits-all answer. The best approach depends on your broader Financial picture, your assets, your health and your long-term plans.

We’ll also be hosting a Pension Briefing in January-keep an eye out for more details, or contact us now to register your interest by emailing [email protected].

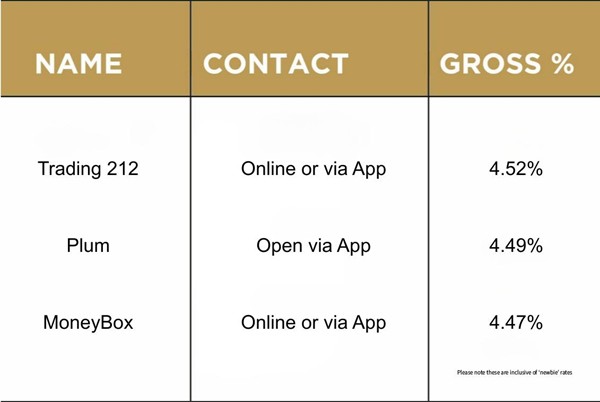

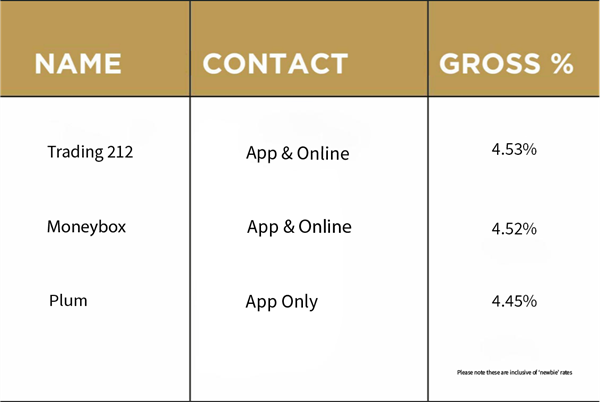

Top three cash ISAs

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial Adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 02/12/2025

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial Adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 05/11/2025