Wealth Management Update October 2025

Making sense of the economy

If you’ve been following the news lately, you could be forgiven for thinking the UK economy is on the brink of collapse. Headlines about rising taxes, immigration pressures and political squabbles don’t exactly paint a rosy picture. But dig a little deeper and there are plenty of reasons to stay positive.

First off, the UK economy is still growing. Forecasts suggest growth of around 1.4% for the year, which actually puts us at the top of the G7 league table. That won’t make the front pages, but it’s good news.

Businesses, particularly small and medium-sized ones, are showing real resilience. In fact, confidence among many UK companies is at its strongest in years, with manufacturing enjoying its best outlook in a decade.

Households are in a mixed spot. Average incomes haven’t really grown since 2019 and inflation has squeezed disposable earnings in recent months. That said, lots of families are still managing to prioritise leisure and holidays, even if they’re tightening the belt elsewhere. Baby boomers, in particular, are happily spending the kids’ inheritance (going ski-ing as we say in Penguin).

The housing market, which many predicted would crash when interest rates rose, has proved surprisingly robust.

Looking ahead, inflation is likely to stay above 3% for a while and food costs could rise further due to global supply pressures. Mortgage rates may edge up slightly as fixed deals expire. But the big picture is that the UK remains a fundamentally stable and innovative economy, with investment in infrastructure and new technology set to boost productivity in the years ahead.

So, what does all this mean for you? In short, don’t let the doom-and-gloom headlines spook you. Yes, there are challenges, but there always are. The key is to focus on what you can control.

Source: HMRC

Lifetime gifting and Inheritance Tax

Inheritance Tax (IHT) is often seen as an unavoidable burden, but with some planning, you can pass on more to your loved ones. The key is making the most of the allowances available and thinking carefully about gifting during your lifetime.

As many of you will already be aware, the main allowance is the nil rate band (NRB), currently £325,000. On top of this, there’s the Residence Nil Rate Band (RNRB), worth up to £175,000 if you’re leaving your home to direct descendants. Combined, that’s potentially £500,000 tax-free per person, or £1m for married couples and civil partners.

When it comes to gifts, there are three main types:

- Exempt gifts – such as those to a spouse or made from surplus income. These are outside IHT completely.

- Potentially Exempt Transfers (PETs) – usually gifts to individuals. They’re tax-free if you survive seven years, but could be pulled back into your Estate if you die sooner.

- Chargeable lifetime transfers (CLTs) – typically gifts into Trusts. These can trigger a 20% charge if they exceed your NRB at the time.

If you die within seven years of a PET or CLT, the NRB is used up by earlier gifts first. Any excess could face 40% IHT. However, there’s some good news: taper relief can reduce the tax if you survive at least three years after the gift and the longer you live, the bigger the savings.

The earlier you start giving gifts, the more effective they can be. As always, the rules can be tricky, so if you’re considering gifting, it’s worth getting our advice to make sure you use the allowances in the best way possible.

Source: HMRC

Interest rates on hold

The Bank of England has kept interest rates at 4%, saying we’re “not out of the woods yet” when it comes to inflation. While inflation has eased from its highs, it’s still running at nearly double the Bank’s target of 2% and that’s why rates haven’t been cut further this time around.

For savers, this means interest rates on savings accounts and cash ISAs are likely to stay relatively attractive, at least for now. On the flip side, anyone with a mortgage coming up for renewal may be hoping for faster cuts, but the Bank is signalling that any further reductions will be gradual and cautious.

Inflation is proving sticky, particularly in everyday essentials. Food prices, for example, are still rising faster than most other goods, with items like beef, milk and butter leading the charge. That puts pressure on household budgets, even though the overall inflation rate has stabilised at 3.8%.

The Bank has cut rates five times since last summer, which shows progress is being made. But two of the nine rate-setters actually voted for a cut at this latest meeting, suggesting we could see lower borrowing costs later in the year if price pressures ease.

So, what does this mean for your Financial Planning? In short, uncertainty remains. Interest rates may fall again, but not dramatically or quickly. Inflation may take longer than expected to reach the 2% target. And with the Chancellor’s Budget coming up in November, there could be more changes around the corner.

Source: Money Policy Committee, Bank of England.

Does the human touch still matter?

You may have seen in the news that some of the big Investment firms are rolling out Artificial Intelligence tools to help their customers. Fidelity, for example, has just launched “Freya”, an AI-powered chat service that can answer questions in real time. It’s clever technology and shows just how quickly the Financial Services world is changing.

But here’s the thing: while AI can be useful for finding quick answers, in our opinion, it can never replace the reassurance of talking to a real person who knows you, your family and your goals. Wealth isn’t just about numbers; it’s about the life you want to live and the people you want to look after. That’s why we believe advice should always have a human touch.

We’re proud to keep that family feel. When you call us, you’ll speak to someone who recognises your voice, not a chatbot. When we sit down together, we take the time to understand not just your Finances, but also your values and what matters most to you. That personal connection means we can give advice that’s truly tailored, not just “personalised” by an algorithm.

At the same time, we’re embracing technology in the right way – using AI and smart systems behind the scenes to help our team work more efficiently, spot opportunities sooner and spend more time where it really matters: with you. It’s humans using technology to give an even better human experience.

Of course, we do use technology to make life easier where we can, but the difference is that our tech supports the process; it doesn’t replace the relationship.

As the Financial world becomes ever more digital, we think keeping things personal is more important than ever. Our promise is simple: we’ll embrace innovation where it helps, but we’ll never lose sight of the human touch that sits at the heart of good service.

Protecting income is more important than ever

The last full week of September was Income Protection Awareness Week, a campaign designed to shine a spotlight on one of the most overlooked types of insurance: protecting your income if you can’t work due to illness or injury.

Now, you might be thinking, “I’m retired, so this isn’t relevant to me.” And that’s true; if you’ve already stopped working, you won’t necessarily need Income Protection yourself. But here’s the thing: it could be hugely important for your children, grandchildren, or anyone in your family who relies on their salary to keep life ticking over.

The cost of living remains high and many households are stretched thin. If someone suddenly lost their income, how would they keep paying the mortgage, covering bills, or supporting their family? Statutory Sick Pay (SSP) is just £116.75 a week – barely enough for food, let alone everything else.

That’s where Income Protection comes in. It provides a regular replacement income if someone can’t work due to illness or injury, giving them breathing space and Financial security when it matters most.

For many families, a loss of income would have a ripple effect. Parents might need to step in to help adult children, or grandparents may end up supporting younger relatives in a crisis. Having proper protection in place helps prevent that burden from falling on loved ones.

You may not need this cover yourself, but encouraging younger generations to think about it could make all the difference. It’s something we help with regularly, so if you’d like to learn more or point a loved one in the right direction, we’d be more than happy to help.

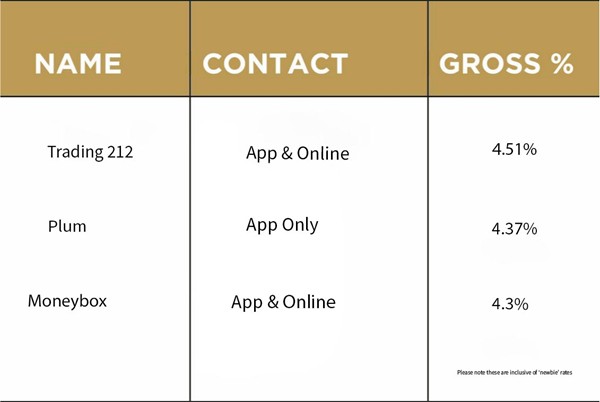

Top three cash ISAs

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial Adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 01/10/2025