The UK received an early Christmas gift with the Bank of England cutting the base rate to 3.75% a few weeks before the big day. While the move was widely expected, it still has important implications as we head into 2026.

For borrowers, this will come as welcome news. Those on variable or tracker Mortgages may start to see their monthly payments edge down, and people approaching the end of a fixed-rate deal could find slightly better options becoming available. That said, lenders tend to move cautiously, so any meaningful relief is likely to be gradual rather than instant. It’s still a good time to review your Mortgage and make sure it suits your circumstances.

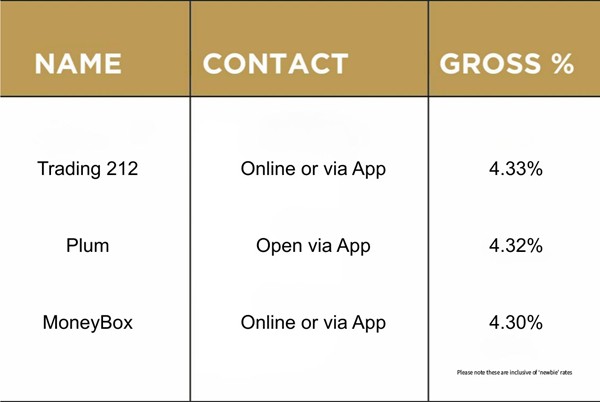

Savers, however, may feel less cheerful. As interest rates fall, returns on cash savings usually follow. With inflation still above target, money left sitting in cash could lose value in real terms over time. Keeping some easy-access cash for emergencies makes sense, but relying on cash alone for longer-term goals may become less effective in a lower-rate environment.

Investors should remember that interest rate cuts often reflect a slowing economy. While markets had already priced in this change, future rate moves will depend on how inflation, wages and growth behave over the coming months. That uncertainty reinforces the importance of diversification and having a long-term Investment plan in place.

With the festive period now behind us, the self-assessment clock is ticking. HMRC expects more than 12 million people to file a tax return for the 2024/25 tax year, but nearly half are still outstanding as the 31 January deadline approaches. If you’re one of them, now’s the time to act.

You’ll usually need to file a return if you were self-employed and earned more than £1,000, sold assets and made a Taxable capital gain, had to repay child benefit through the High- Income Child Benefit Charge, or were part of a business partnership. Even if none of these apply, you may still need to file if you received more than £10,000 in savings or Investment income.

One common trap is assuming you don’t need to file just because you’re Taxed through PAYE or think there’s no Tax to pay. That’s only true if HMRC has confirmed this or you’ve told them about any changes. If HMRC has asked you to complete a return and you ignore it, penalties can still apply.

This Tax year also comes with a few quirks. Capital gains Tax rates changed partway through the year, which means extra care is needed if you sold Investments after 30 October 2024. Child benefit thresholds also increased, but repayment may still be due if your income was high enough and your Tax code wasn’t adjusted.

A note on savings interest and Simple Assessments:

One extra wrinkle to be aware of this year is bank and building society interest.

From October 2025, HMRC will have started issuing Simple Assessment letters to collect any Tax owed on savings interest earned between April 2024 and April 2025. This applies where HMRC believes Tax is due but you’re not already filing a Self-Assessment return.

In some cases, HMRC may issue more than one Simple Assessment letter for the same Tax year. This can happen if they receive interest information later from banks or building societies. If that happens, the second letter shows the total Tax owed for the year, including any amount shown on the first letter – even if you’ve already paid it. To work out what’s still due, you simply deduct anything you’ve already paid from the latest figure.

It’s also worth noting that figures can differ from what you expect. That’s because:

Most people can earn some interest Tax-free, and depending on your Tax band, you may be able to earn up to £1,000 a year in interest without paying Tax. If you haven’t used your full Personal Allowance elsewhere (for example on wages or pension income), this can also be set against savings interest.

If you receive a Simple Assessment, the letter will explain how much you owe and how to pay. If you think it’s wrong, you must contact HMRC within 60 days to formally dispute it. If you’ve already registered for Self-Assessment for that year, HMRC can withdraw the Simple Assessment instead.

Finally, don’t forget payment. Any Tax owed must be paid by 31 January 2026 to avoid interest and penalties.

There’s some good news on the Inheritance Tax front for Business Owners and Farmers. Ahead of changes due in April 2026, the government has confirmed an important amendment that makes the new rules far more generous and manageable than first feared.

From 6 April 2026, a new £2.5 million allowance, increased from the original £1 million, will apply to assets that qualify for Agricultural Property Relief and Business Property Relief at 100%. This means up to £2.5 million of qualifying business or agricultural assets can still pass on free from Inheritance Tax. Anything above that level will continue to benefit from relief, just at a reduced rate, resulting in an effective 20% Inheritance Tax charge rather than the full 40%.

Crucially, this allowance applies to both lifetime gifts and assets held on death, and it is refreshed every seven years. Any unused allowance can also be passed to a spouse or civil partner, meaning that on second death, provided the allowance wasn’t used on first death, £5 million can pass down and receive 100% relief.

Another positive change is flexibility around paying any Tax due. Where Inheritance Tax does apply, families will be able to spread payments over up to ten annual instalments, interest-free, easing pressure on cashflow and reducing the risk of assets needing to be sold quickly.

Getting married is usually fairly romantic, but for a growing number of older couples, upcoming tax changes mean that saying “I do” is also becoming a very practical Financial decision, even if it’s not the most romantic motivation.

From April 2027, Pensions are due to be included in Taxable Estates for Inheritance Tax. For married couples and civil partners, Pensions can usually pass to a surviving partner without an Inheritance Tax bill. For unmarried couples, that protection doesn’t apply in the same way. As a result, some long-term partners are realising that marriage could significantly reduce their Tax burden on death.

There are, however, some points to consider if this route takes your fancy. Marriage automatically cancels an existing Will, which can create unintended consequences if it isn’t replaced quickly. Planning structures that once worked well for cohabiting couples may also no longer deliver the protection families expect. This is why many older couples are

now taking extra steps before tying the knot. Prenuptial or postnuptial agreements are increasingly common, helping to ringfence assets and Pensions built up before marriage. Updating Wills, reviewing Pension death benefit nominations and revisiting Inheritance Tax planning are all essential parts of the process.

While choosing marriage for Tax reasons may not sound particularly romantic, it’s something we discuss far more often than you might expect. We regularly advise couples who have been together for many years but never quite felt the need to spend money on “a party” or a piece of paper. When we explain the potential Tax advantages, many decide that – if nothing else – it’s a practical step worth taking. In that context, perhaps “till Tax do us part” does deserve a quiet mention in the vows.

Market ups and downs are expected to be a bigger feature of Investing in 2026, especially with our tango friend still causing chaos. It’s completely natural to feel a little uneasy when headlines turn noisy. The key thing to remember is that volatility, while uncomfortable, is a normal part of Investing for long-term growth.

Periods of uncertainty are being driven by a mix of factors, including the global economic outlook, inflation and interest rate decisions. These forces can cause short-term swings in Investment values, but they don’t necessarily change the long-term reasons you’re Invested in the first place.

One risk during volatile markets is reacting too quickly. Selling Investments when markets fall can turn temporary drops into permanent losses, while staying out of the market for too long can mean missing the recovery. This is where having a clear plan really matters. Your Investment strategy should already reflect your goals, time horizon and attitude to risk, so short-term market movements don’t need to drive big decisions.

Most importantly, volatile markets are a time for conversation, not panic. Reminding yourself of your long-term objectives can provide reassurance when markets feel unsettled.

Please check the terms and conditions before opening any account. If in doubt, consult with your financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 07/01/2026

Penguin © 2026. Penguin is a trading name of Penguin Wealth Planners Ltd. who are authorised and regulated by the Financial Conduct Authority (FCA no. 830057). For further information please View More

Customer Focus Award

Customer Focus Award