Recent HMRC figures show that £61 million worth of so-called “gifts” were pulled back into Estates last year under the gift with reservation of benefit (GWRoB) rules.

What does that mean in practice? Essentially, it’s when you say you’ve given something away but continue to use it yourself. A common example is parents “gifting” their home to their children, but still living there rent-free. HMRC doesn’t see that as a gift at all and the property remains liable for Inheritance Tax when the parents pass away.

This is a common mistake. Families feel they’ve outsmarted the system, children believe they’ve inherited early and parents continue with life as usual. Unfortunately, when the time comes, the Estate still gets hit with a hefty Tax bill.

The GWRoB rules are one of the simplest traps to fall into, but with the right planning, they’re also easy to avoid. Lifetime giving can be a fantastic Inheritance Tax strategy, provided it’s done properly. That usually means:

We know it feels less straightforward than simply passing on the keys, but Inheritance Tax planning rarely rewards shortcuts. Done correctly, it can save your family thousands and give you the peace of mind that your intentions will stick.

If you’d like to avoid the common traps and gift with real confidence, download our Trust Guide or speak to one of our Financial Advisers by calling us on 02920 450143 or email [email protected] to explore the right structure for your plans.

The Government has now confirmed the outcome of its consultation on how unused Pensions and Death Benefits will be treated for Inheritance Tax (IHT) from April 2027.

At present, most Pension funds can be passed on free of IHT. From April 2027, unused Pension funds and some Lump Sum Death Benefits will generally be included in the value of a Person’s Estate, which could increase the Tax bill.

There is some good news. All Death-in-Service benefits will remain outside the scope of IHT, including those within registered Pension schemes. This is particularly welcome for members of NHS and other public sector schemes, which are currently treated less favourably. The Government has also confirmed that you will not be Taxed twice. Where IHT is due on a Pension, the same amount will not also be subject to Income Tax.

A major focus of the consultation was on who should be responsible for reporting and paying the Tax. The original suggestion was that Pension scheme administrators would handle this, but that idea has been dropped. Instead, responsibility will rest with the personal representatives of the deceased’s Estate, as it does for other assets.

This change will make Estate Planning more complex. If Pension beneficiaries are different from the rest of the Estate, personal representatives may face challenges in finding the funds to pay IHT before Probate can be granted.

With April 2027 approaching, now is the right time to review your Estate plans. Taking Advice early will help ensure your Pensions, which are often one of your largest assets, are passed on as efficiently as possible.

We’re planning to run briefings on these changes later this year or early next, once the next Budget has been announced. If you’d rather speak with someone sooner, please don’t hesitate to call us on 02920 450143 or email [email protected] to arrange a conversation.

Not all Trusts are created equal – and the Government’s latest response to its consultation on the Trust Registration Service (TRS) recognises that.

In a welcome move, new rules will ease the red tape for certain small, low-risk Trusts, while keeping transparency where it matters most. From around April 2026, a new exemption will apply to new non-Taxpaying Trusts that meet all of the following conditions:

If a Trust exceeds any of these thresholds in the future, it will need to register and will remain registered thereafter.

A key point to note: this exemption will apply only to new Trusts created after the rules come into force.

Existing Trusts – including many of the familiar “£10 pilot Trusts” – will still need be registered under the current TRS rules.

For now, nothing changes. The current TRS requirements remain in place until the new rules come into force.

If you already have a Trust or are thinking about setting one up, it’s worth reviewing your arrangements now to stay compliant and avoid unnecessary hassle later.

If you’d like to understand what these changes could mean for you or your family’s plans, our team at Penguin is here to help. Simply get in touch and we’ll talk it through together.

With unused Pension savings set to fall within the Inheritance Tax (IHT) net from April 2027, many families will face larger Tax bills on death. One option that some families consider is Gift Inter Vivos insurance. Professional Advice is essential to determine whether this type of cover is suitable.

GIV cover is a specialist form of Life Insurance designed to protect against the potential IHT liability that can arise when a large gift is made during someone’s lifetime. If the donor passes away within seven years of making the gift, IHT may be due. A GIV policy provides a way of covering that risk, ensuring beneficiaries are not left with an unexpected bill.

The cover is written on the life of the donor and the sum insured reduces each year to mirror the taper relief rules that gradually reduce the IHT liability. Policies usually last for seven years, although shorter terms can be arranged to reflect earlier gifts.

This type of policy is particularly useful where the recipient of a gift may not have the funds to pay an IHT bill themselves. By putting cover in place, donors can make meaningful gifts during their lifetime while ensuring those gifts are received in full.

When considering GIV insurance, it is important that the policy is written in Trust for the intended beneficiaries and that the level and length of cover are appropriate. Costs will depend on age, health and the value of the gift. Professional Advice can help ensure the policy is structured correctly and provides peace of mind for both you and your family.

The Autumn Budget is one of the most important events of the year for savers and investors and speculation is already building around what the Chancellor may announce later this year.

Some of the main areas under discussion are ISAs, Pensions, Inheritance Tax and capital gains Tax. At this stage, though, it is worth stressing that these are only rumours. Making Financial decisions based on speculation can prove costly, as we saw last year when some people rushed to take Pension lump sums after rumours about changes to Tax-free cash, changes which never materialised.

ISAs are currently under review, with the Government exploring whether the balance between cash and stocks and shares is right. This could result in changes to ISA limits, although nothing has yet been confirmed. There is also talk of possible adjustments to salary sacrifice arrangements for Pensions and the way Tax relief works on contributions. Inheritance Tax may also come back into focus, particularly around lifetime gifts and the nil- rate band, which has been frozen since 2009. Capital gains Tax, too, could be revisited after recent rate increases and allowance cuts.

What does this mean for you? For now, the best approach is to keep calm and avoid hasty decisions. A well-structured Financial Plan should be able to accommodate change without the need for sudden action. When the Chancellor does reveal the detail in the Autumn, we will be ready to review the measures and guide you on how they affect your long-term plans.

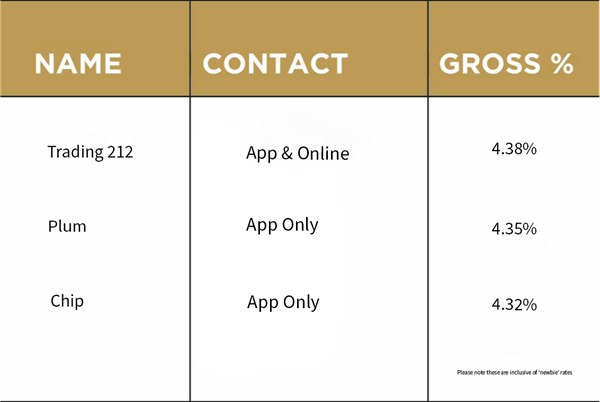

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial Adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 01/09/2025

Penguin © 2026. Penguin is a trading name of Penguin Wealth Planners Ltd. who are authorised and regulated by the Financial Conduct Authority (FCA no. 830057). For further information please View More

Customer Focus Award

Customer Focus Award