You may have seen recent headlines about Pensions and Inheritance Tax following the Finance Bill receiving Royal Assent on March 18, 2026.

For years, Pensions have been seen as one of the most Tax-efficient ways to pass on wealth. In many cases, they’ve sat outside Estates for Inheritance Tax (IHT), making them a useful planning tool.

However, changes first announced in the 2024 Budget are now set to definitely shift that position. The Government plans to bring Pension funds into the IHT net, meaning they will be included when calculating the value of Estates on death.

This could have a noticeable impact. Projections suggest that more than 60,000 Estates a year may face an Inheritance Tax liability by 2031, reflecting a steady rise in the number of families affected.

In simple terms, this means Pensions may no longer be quite as sheltered from Inheritance Tax as they once were. If unused Pension funds are counted as part of estates, it could increase the overall Tax bill passed on to Beneficiaries.

That said, Pensions remain a highly valuable part of Financial planning. These changes are more about how wealth is treated after death than about reducing the benefits of saving into a Pension during one’s lifetime.

We will also be holding a Pension & IHT briefing at 10am on 11th June, where we’ll be covering these changes and what they may mean for clients in more detail. Please keep your eyes peeled for further information regarding the briefing, which will be shared soon.

Gifting money or assets to family and friends is something many people do with the best of intentions. Whether it’s helping children onto the property ladder or supporting loved ones day-to-day, it can feel like a positive and straightforward decision.

However, recent research from Canada Life suggests there’s a potential issue many people aren’t aware of. More than half (54%) of over-55s who have given Financial gifts in the last seven years have not kept any record of them. Only 13% said they stored this information securely, while others relied on informal notes, or nothing at all.

This becomes important when it comes to IHT. When someone dies, their Estate must be reported to HMRC along with the details of gifts made in the seven years before death. Without accurate records, this process can become much more difficult.

Put simply, if there’s no clear record of what was given, when, and to whom, Executors may struggle to complete the paperwork properly. That can lead to delays, additional questions from HMRC, and unnecessary stress for family members at an already difficult time.

Another common issue is that many people don’t realise what counts as a “gift” for IHT purposes. It’s not just cash, items like jewellery, furniture, shares, or even property can all fall within the rules.

The research also found that people may be giving away significant sums without fully tracking them. Among those who could estimate, the average gifted over seven years was £42,056, far above the standard annual gifting allowance.

In short, generosity is a wonderful thing, but keeping a clear record of it can make a big difference later on.

If you would like a copy of our Penguin Gift Tracker or our Gift Out Of Income Tracker to help keep accurate records, please feel free to email us and we’ll be happy to send these across.

Big changes are on the horizon for ISA savers, and they could have a noticeable impact on how you use your annual allowance.

From 6 April 2027, the amount you can put into a cash ISA each year is expected to fall from £20,000 to £12,000. The overall ISA allowance stays the same, but the remaining £8,000 will need to go into Investments like a stocks and shares ISA.

Recent analysis highlights why these matters. Looking back over the last decade, someone who invested £8,000 in global equities and kept £12,000 in cash could now have around £41,100. By comparison, keeping the full £20,000 in cash would have resulted in around £24,000.

The difference becomes even more striking when looking at full Investment. A £20,000 Investment in global equities over the same period could now be worth roughly £66,700, more than £42,000 higher than cash savings alone.

Inflation also plays a key role. Over that time, £20,000 would need to grow to about

£28,200 just to keep pace with rising prices. Cash savings alone would have fallen short of that, while Investments would have comfortably exceeded it.

None of this means cash ISAs are no longer useful. They still play an important role, particularly for short-term needs or emergency funds.

It is also worth remembering that you can transfer money from a cash ISA into a stocks and shares ISA without losing your current ISA allowance, provided the transfer is completed through the ISA transfer process rather than withdrawing the money yourself.

If you would like to discuss what these potential changes could mean for your savings and Investments, or whether your current ISA strategy is still right for you, please contact your Adviser.

Inflation is back in the headlines, with the latest figures showing prices rising by 3.3%. While that’s well below the peak of over 11% seen in 2022, it still has a real impact on everyday Finances.

It can feel like prices are only going one way, but inflation doesn’t always move in a straight line. Some recent factors, like a temporary drop in the energy price cap, are expected to ease pressure slightly in the short term.

However, there are signs this could be temporary. Energy bills are expected to rise again later in the year, and while fuel prices have dipped a little, they’re still significantly higher than before recent global tensions. Expectations are that inflation could dip below 3% briefly, before potentially rising towards 4% later this year.

Inflation plays a big role in decisions made by the Bank of England. Its goal is to keep inflation around 2%, but the current picture is uncertain.

The Bank of England has kept interest rates at 3.75%, which was widely expected, but the bigger story is what might happen next.

While most of the committee voted to hold, one member, pushed for an immediate rise. More importantly, the Bank made it clear that further increases are likely and could be quite “forceful” if inflation picks up.

So, what’s driving this? In short, uncertainty. The ongoing situation in the Middle East is having a big impact on energy prices, which in turn affects inflation. As Andrew Bailey put it, things are moving quickly and unpredictably, especially oil prices.

The Bank has looked at a range of possible outcomes, from a relatively mild increase in inflation to a much more serious scenario where inflation rises above 6% and interest rates climb sharply. Right now, they seem to expect something in the middle, but there are no guarantees.

Borrowing costs could still rise, and Mortgage rates may remain higher for longer than many had hoped.

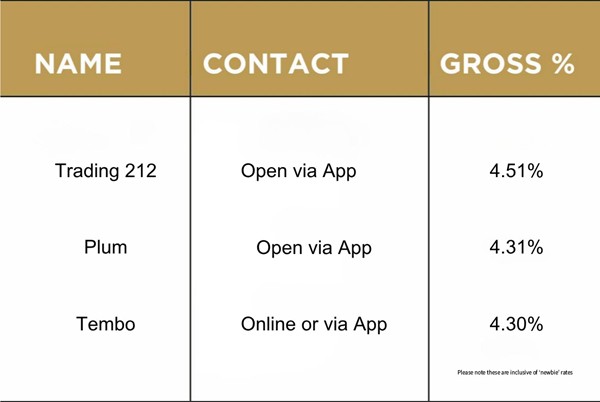

Please check the terms and conditions before opening any account. If in doubt, consult with your Financial adviser directly, as the above is for your information only.

Source: Moneysavingexpert.com 05/05/2026

Penguin © 2026. Penguin is a trading name of Penguin Wealth Planners Ltd. who are authorised and regulated by the Financial Conduct Authority (FCA no. 830057). For further information please View More

Customer Focus Award

Customer Focus Award